You have 0 items in your cart

By George Okenyo Omwansa, Founder & Lead Advocate Okenyo Omwansa & Co. Advocates, Nairobi Published: March 2026

As of March 2026, Kenya’s tax system stands at a pivotal moment. The National Treasury, led by Cabinet Secretary John Mbadi, and the Kenya Revenue Authority (KRA) are pushing forward with reforms aimed at two core goals: providing meaningful relief to low- and middle-income earners struggling with the cost of living, while simultaneously tightening digital compliance to close revenue leakages and expand the tax base.

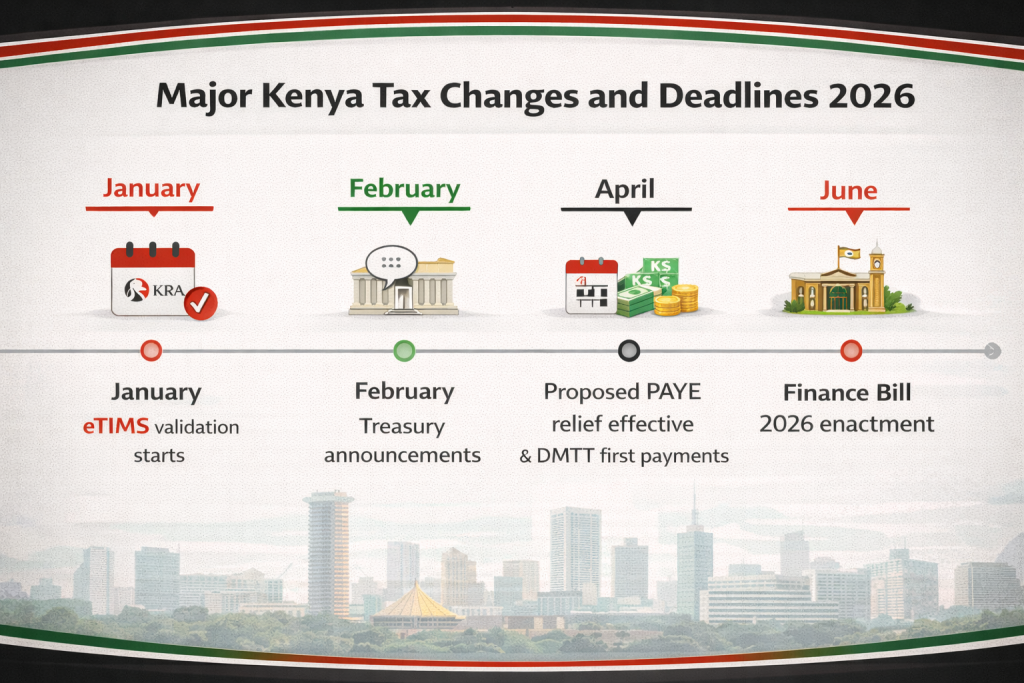

The centerpiece proposals appear in the anticipated Tax Laws (Amendment) Bill 2026 (signaled for tabling as early as February 2026) and the broader Finance Bill 2026 (draft expected by end-April 2026, with enactment targeted for June). These build directly on the 2026 Budget Policy Statement, the Medium-Term Revenue Strategy (MTRS) targeting a higher tax-to-GDP ratio (around 20%), and ongoing implementation of prior laws like the Finance Act 2025.

Many elements remain proposals at this stage—they require vigorous parliamentary debate, public participation, and presidential assent before becoming binding law. As advocates practicing in Nairobi, we regularly represent clients in PAYE disputes, corporate income tax audits, transfer pricing reviews, and eTIMS compliance challenges. We’ve seen firsthand how these shifts can create savings for employees and added burdens (or strategic opportunities) for businesses.

This comprehensive guide breaks everything down clearly, with practical implications, real examples from our practice, and actionable steps you can take right now.

1. PAYE Relief – The Headline Proposal for Salaried Kenyans

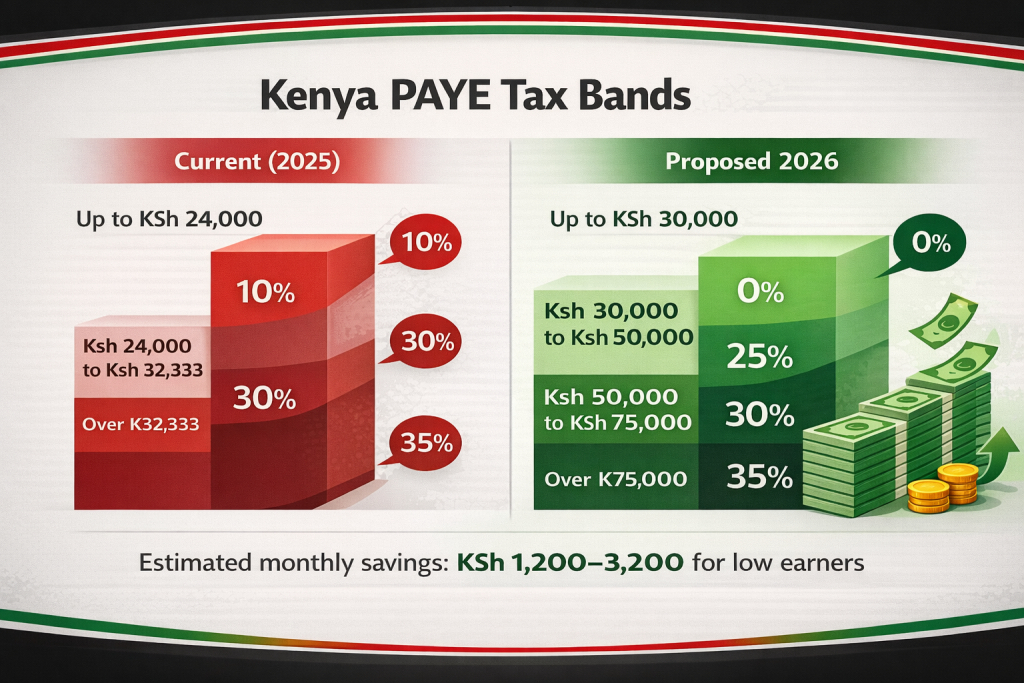

Treasury CS John Mbadi announced in early February 2026 that the government plans to exempt monthly earnings up to KSh 30,000 from Pay-As-You-Earn (PAYE) income tax. This would raise the effective zero-tax threshold from the current ~KSh 24,000 (after personal relief). President William Ruto has publicly endorsed the move, framing it as direct support for households facing high living costs under the Bottom-Up Economic Transformation Agenda.

The next income band (KSh 30,001 to KSh 50,000) would face a reduced rate of 25% instead of the current 30%. Higher bands may see a cap or modest adjustments, though details remain fluid.

Proposed vs Current PAYE Structure (Monthly – Subject to Final Enactment)

| Monthly Gross Income | Current Bands & Effective Rate (after KSh 2,400 personal relief) | Proposed 2026 Structure | Estimated Monthly Net Gain Example (approx.) |

|---|---|---|---|

| Up to KSh 30,000 | Progressive 10–30% on portions after relief | 0% (full exemption proposed) | KSh 1,200–3,200 (depending on exact band) |

| KSh 30,001 – KSh 50,000 | 30% on the portion above lower bands | 25% on this KSh 20,000 slab | KSh 1,000–2,100 |

| Above KSh 50,000 | 30–35% on higher portions (varies by old slabs) | Likely 30% cap proposed (pending) | Variable; modest relief possible |

Personal relief (KSh 2,400/month) is expected to continue, but its interaction with the new zero band is still under discussion—some analysts question whether it might be adjusted or phased out to simplify calculations.

Real-World Impact for Employees

Consider a common Nairobi scenario: a primary school teacher or entry-level bank teller earning KSh 28,000 gross monthly. Under current rules, after relief and statutory deductions (NSSF Tier I/II, SHIF, Affordable Housing Levy), PAYE might deduct KSh 1,500–2,500. The proposal could eliminate that entirely, putting an extra KSh 18,000–30,000 annually back in their pocket.

That money typically goes straight into essentials: matatu fares, school uniforms, market vegetables, or small emergency savings. Treasury estimates suggest around 1.5 million of Kenya’s ~3 million formal employees could benefit from full exemption, aligning with efforts to boost disposable income and stimulate local consumption.

However, Treasury PS Chris Kiptoo cautioned in February 2026 statements that meaningful relief hinges on expanding the tax base—bringing more informal-sector participants and non-compliant businesses into the formal system. Without that, aggressive cuts could strain public finances, potentially leading to delayed implementation or offsets elsewhere (e.g., higher indirect taxes).

Our advice for individuals (March 2026):

- Model your current payslip against the proposed bands using free online calculators or your HR system’s test mode.

- If your employer hasn’t started planning, ask about their timeline—many large firms update payroll software quarterly.

- Keep records of payslips; discrepancies during transition could trigger KRA queries.

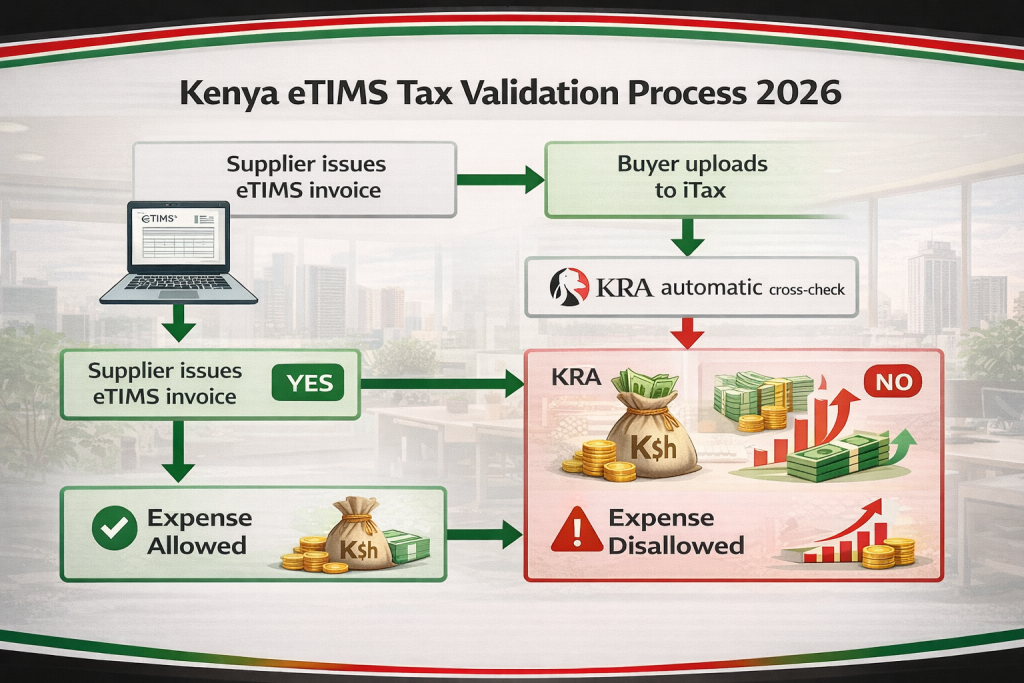

2. eTIMS Validation – The Enforcement Shift Already Live

While PAYE relief dominates headlines, the most immediate and disruptive change for businesses is the full activation of eTIMS-based validation starting 1 January 2026.

KRA now cross-checks declared income and expenses in 2025 year-of-income returns (filed throughout 2026) against real-time data from:

- eTIMS / TIMS electronic invoices

- Withholding tax certificates

- Customs import declarations

Core legal basis: Finance Act 2023 amendments to the Income Tax Act disallow expenses unless supported by electronic invoices (per Tax Procedures Act s.23A and Tax Procedures (Electronic Tax Invoice) Regulations, 2024). KRA’s November 2025 public notice confirmed automated validation begins January 2026—no more manual overrides for most cases.

Exceptions remain (salaries/emoluments, certain imports, final withholding taxes, airline ticketing), but the vast majority of operating costs (rent, supplies, professional fees, marketing, transport) now require a valid eTIMS invoice transmitted with the buyer’s PIN.

Who Feels the Pain Most?

- SMEs and informal traders relying on cash or handwritten receipts.

- Importers and wholesalers with partial supplier compliance.

- Professionals (consultants, lawyers, doctors) using manual subcontractor billing.

- Rental property owners and Turnover Tax (TOT) filers with undocumented costs.

In our practice, we’ve run simulations for clients showing 20–40% of claimed expenses at risk. One mid-sized Nairobi logistics company (trucks, fuel, repairs) projected a KSh 4–6 million jump in taxable profit after disallowing unmatched invoices—translating to KSh 1.2–1.8 million extra tax at 30%, plus potential interest/penalties if audited.

Broader consequences:

- Phantom profit taxation — You pay 30% corporate (or personal) tax on expenses that were genuinely incurred but undocumented.

- TCC linkage — Tax Compliance Certificates now require eTIMS registration; no compliance means lost government tenders, bank loans, or contracts.

- Audit triggers — Mismatches between your iTax return and KRA’s datasets can prompt automatic notices or full audits.

Practical steps businesses should take now (March 2026):

- Request eTIMS income/expense schedules from your KRA account manager (feature rolling out).

- Audit top 20–30 suppliers—demand eTIMS invoices or switch vendors.

- Integrate eTIMS into your accounting software (QuickBooks, Sage, ERP systems have plug-ins).

- Add compliance clauses to new contracts (“Supplier shall issue eTIMS invoices with Buyer PIN”).

- Reconcile 2025 records before filing—fix gaps to avoid disallowances.

Early movers avoid surprises; late filers face higher costs.

3. Other Major 2026 Reforms – Global Alignment & Incentives

Beyond PAYE and eTIMS, several reforms round out the 2026 picture.

Domestic Minimum Top-Up Tax (DMTT / QDMTT)

Introduced via Finance Act 2025 (effective 2025 income years), aligned with OECD Pillar Two. Multinational groups (≥€750m global consolidated revenue) must ensure a 15% effective tax rate in Kenya. Top-up payable by the fourth month after year-end (e.g., April 2026 for Dec 2025 FY).

Draft regulations (Nov 2025) clarify GloBE calculations, safe harbors, and filing. First real payments loom in 2026—groups must run models now.

Note: Kenya granted a political (not statutory) exemption for certain U.S.-headquartered tech firms following bilateral talks, sparking debate on revenue fairness and AfCFTA implications.

Nairobi International Financial Centre (NIFC) Incentives

Qualifying firms (meeting investment thresholds) enjoy 15% corporate tax for 10 years—still attractive for new entrants in finance, tech, or green projects.

Advance Pricing Agreements (APAs)

Effective 1 January 2026 via Finance Act 2025 and draft regulations (Nov 2025). Multinationals with related-party transactions can lock in transfer pricing methods for up to 5 years, reducing audit risk and providing certainty.

Our experience: Clients applying early avoid lengthy disputes—APA process takes 6–18 months, so 2026 is prime time to initiate.

VAT & Other Discussions

Proposals for VAT drop to 15% (from 16%) surfaced but remain conditional on revenue performance—no confirmation yet.

Why Act in March 2026? The Preparation Window

Parliamentary debate on the Finance Bill could stretch into mid-2026. Use this time wisely:

- Employees: Simulate new take-home pay; discuss with HR.

- Businesses: Complete eTIMS supplier onboarding; run disallowance scenarios; explore APAs/DMTT modeling.

- Everyone: Monitor Treasury/KRA websites and Parliament hansards.

These reforms balance relief with enforcement. Done right, they support growth; mishandled, they raise compliance costs.

Frequently Asked Questions – March 2026 Status

Is PAYE zero up to KSh 30,000 guaranteed? Proposed and widely supported, but not law yet—await Bill passage and assent.

What happens if a supplier refuses eTIMS? Formally request it; document refusal; consider alternative suppliers. KRA holds the buyer accountable for unmatched expenses.

Are very small businesses exempt from eTIMS validation? Limited exemptions apply (e.g., below thresholds), but most must comply—check latest KRA notices.

How does DMTT affect non-multinationals? It doesn’t—only groups meeting the €750m global threshold.

For a personalized, no-obligation assessment of how these Kenya tax changes 2026 proposals impact your salary, payroll, business deductions, or multinational structure, reach out today. We offer quick reviews and compliance roadmaps.

Contact Okenyo Omwansa & Co. Advocates – Let’s keep you ahead.